2010년 11월 27일 토요일

2010년 11월 26일 금요일

Creating a Warrant Market Making Engine

http://www.asiaetrading.com/creating-a-warrant-market-making-engine/

http://dolppi.egloos.com/1631932

http://dolppi.egloos.com/1631932

1. 배경

1) warrant trading이 굉장히 고수익이 났었지만, 점점 수익을 내기 어려워졌음

- 너무 많은 player들이 있음

- algorithm 이 많이 들어옴. IT 예산만 있으면 최신 제품을 들여올 수 있음

- 시장 변동성이 커져 hedging이 점점 비싸고 어려워짐

2) warrant 비즈니스의 성공을 위해서는

- 최대한 많은 warrant를 투자자들에게 공급해야함

- 적절한 기술을 도입해 best price와 liquidity를 공급해야만 투자자의 관심을 끌 수 있음

- market making에 고유한 risk와 exposure를 적절히 관리해야함

2. market making engine이 왜 필요할까?

아래 질문들에 대한 대답이 YES가 많다면 market making engine이 필요하다.

1) 트레이더들이 여전히 수동 주문을 사용하는가?

2) 모든 active outstanding warrant를 관리하는데 어려움을 느끼고 있는가?

3) warrant를 더 많이 발행해 규모를 늘일 계획이 있는가?

4) ETF warrant를 발행할 계획이 있는가?

5) market making에 대한 아이디어는 많은데 시스템이 못따라주고 있는가?

6) 트레이더들이 misprice 로 가끔 손실이 발생하는가?

7) mispriced warrant를 발견했지만, 시장에서 이미 누군가가 매매해버리는가?

3. market making engine을 어떻게 가질수 있나?

1) off the shelf. 최신 제품을 구매한다.

- 많은 벤더들이 "즉시 구매, 즉시 사용가능"을 강조한다. 하지만,

- 커스터마이징, 컴플라이언스 및 risk 관리 연결, 내부 시스템 연결 등 할 일이 많다

- 가장 큰 문제는 벤더 제품을 구매한다고 해서 경쟁력이 높아지지 않음. "누구나 사용하고 있기 때문에"

2) in-house. 직접 개발.

- 직접 개발하면 "tailor-made"처럼 트레이더들의 요구에 잘 부합할 것 같다.

- 벤더 제품처럼 사용료나 개발비 등을 지불하지 않아도 된다.

- 트레이딩 기술 역시 노출되지 않는다.

- 하지만, market making engine은 직접 개발하기에 만만한 기술이 아니다.

- "개발자들이 market making business 에 대해 이해도가 높은가?"

- "개발자들이 Complex Event Processing (CEP) 기술에 대해 잘 아는가?"

- "개발자들이 auto-trading system을 개발할만한 지식이 있는가?"

- 직접 개발하면 수개월, 혹은 수년이 걸리더라도 끝이 안 날 가능성이 있다는 것을 명심해야 함

3) combination. 적절한 벤더를 선택해 공동으로 개발한다.

- 전문가를 보유하고 있는 적절한 벤더를 선택

- 알고리즘 트레이딩 기술을 보유하고 있는 벤더를 선택하는 것이 유리하다.

- 공동으로 개발하면서 기술 이전을 받는다.

4. market making engine은 무엇인가?

1) market making engine은 외부 이벤트에 대해 반응하면서 적절한 action을 취하는 것.

2) market making engine에 필요한 events

- 시세 이벤트

- 거래 이벤트 (신규/정정/취소주문, 체결)

- 사용자에게서 발생하는 이벤트 (매도/매수 주문 실행, 변동성이나 스프레드 같은 parameter 변경)

- 시스템 이벤트 (시장 상황, 시스템 상태, 네트워크 링크 등)

3) 이벤트에 대응하는 action

- fair value pricing 및 내재변동성 계산

- 매수/매도 주문 정정/취소

- individual and overall exposure 계산

- trade misprice opportunities in the market

- 사용자 최종 상태 업데이트

- quoting 시작/중지

5. market making engine이 제공해야 하는 기능

1) 대량의 데이터를 다른 시스템에 부하없이 처리

2) 실시간으로 warrant의 fair value 등에 대해 평가하고 계산

3) "low latency" 시세 데이터 처리

4) high volume trading - 수십/수천 개의 주문을 동시에 발주

5) 다양한 전략을 지원하는 아키텍쳐

6) GUI - 트레이더가 쉽게 모니터링하고 market making 전략을 수정할 수 있어야

7) GUI - 트레이더가 쉽게 커스터마이징 할 수 있어야

8) 대량의 손실을 피하기 위한 장치

9) greeks 에 대한 모니터링, auto-hedging. 자전거래(self-matching) 피해야.

6. 결론

1) market making engine을 개발하는 것은 사소한 일이 아님. 신중한 접근이 필요.

2) 위의 방식들 각각 장/단점이 있음

3) warrant market making engine은 수천의 데이터를 보고, 미리 정의된 알고리즘에 따라 즉각적으로 반응

4) warrant 비즈니스는 아시아에서 확대되고 있고, 많은 거래소들에서 상장하고 있음

5) warrant market making은 아시아에서 수익성이 있고, 특히 Thai 같은 신규시장에서 가능성이 높음.

거래소, 오는 29일 경쟁대량매매제도 본격 시행

http://www.asiae.co.kr/news/view.htm?idxno=2010112211013719171

[아시아경제 김유리 기자]한국거래소(KRX)는 오는 29일부터 정식으로 경쟁대량매매제도를 시행할 것이라고 22일 밝혔다.

경쟁대량매매는 익명거래를 원하는 투자자의 일정규모 이상 되는 호가를 정규시장 매매와 별도로 집중시켜 매매를 체결시키는 방식이다.

최소호가규모는 유가증권시장의 경우 5억원, 코스닥시장은 2억원 이상으로 한정됐다. 매매수량단위는 거래편의와 매매효율성을 고려해 100주로 조정됐다. 코스닥시장의 경우 1주다.

경쟁대량매매는 주식(DR 포함)과 ETF에 한해 허용된다. 관리종목이나 정리매매종목은 대상에서 제외된다.

매매 방법은 상대주문이 있는 경우 즉시 매매를 체결하는 연속매매(접속매매) 방식이다. 오전 7시30분부터 1시간 동안 장개시전 시간외시장 및 오전 9시부터 오후 2시30분까지 정규시장 중 매매를 체결하게 된다. 장종료 후 시간외시장은 제외된다.

호가제출·매매체결 등의 과정에서 거래 익명성이 유지되도록 호가수량 및 체결 정보는 미공개로 하되 종목별로 경쟁대량매매를 위한 매수·매도 호가의 유무 정보는 정규시장 중에 한해 공개하게 된다.

경쟁대량매매를 통한 체결정보 역시 시장에는 공개하지 않고 거래당사자(해당 회원 및 투자자)에게만 체결시점에 실시간으로 통보한다. 단 체결가격은 정규시장 종료후 거래량가중평균가격으로 별도 통보한다.

거래소 관계자는 "경쟁대량매매제도가 시행 되면 자산운용사 등 기관투자자는 물론 개인투자자도 5억원(코스닥은 2억원)이상 대량거래를 하는 투자자라면 누구든지 자신의 주문정보 노출 없이 편리하게 대량거래를 할 수 있을 것"이라고 기대했다.

[아시아경제 김유리 기자]한국거래소(KRX)는 오는 29일부터 정식으로 경쟁대량매매제도를 시행할 것이라고 22일 밝혔다.

경쟁대량매매는 익명거래를 원하는 투자자의 일정규모 이상 되는 호가를 정규시장 매매와 별도로 집중시켜 매매를 체결시키는 방식이다.

최소호가규모는 유가증권시장의 경우 5억원, 코스닥시장은 2억원 이상으로 한정됐다. 매매수량단위는 거래편의와 매매효율성을 고려해 100주로 조정됐다. 코스닥시장의 경우 1주다.

경쟁대량매매는 주식(DR 포함)과 ETF에 한해 허용된다. 관리종목이나 정리매매종목은 대상에서 제외된다.

매매 방법은 상대주문이 있는 경우 즉시 매매를 체결하는 연속매매(접속매매) 방식이다. 오전 7시30분부터 1시간 동안 장개시전 시간외시장 및 오전 9시부터 오후 2시30분까지 정규시장 중 매매를 체결하게 된다. 장종료 후 시간외시장은 제외된다.

호가제출·매매체결 등의 과정에서 거래 익명성이 유지되도록 호가수량 및 체결 정보는 미공개로 하되 종목별로 경쟁대량매매를 위한 매수·매도 호가의 유무 정보는 정규시장 중에 한해 공개하게 된다.

경쟁대량매매를 통한 체결정보 역시 시장에는 공개하지 않고 거래당사자(해당 회원 및 투자자)에게만 체결시점에 실시간으로 통보한다. 단 체결가격은 정규시장 종료후 거래량가중평균가격으로 별도 통보한다.

거래소 관계자는 "경쟁대량매매제도가 시행 되면 자산운용사 등 기관투자자는 물론 개인투자자도 5억원(코스닥은 2억원)이상 대량거래를 하는 투자자라면 누구든지 자신의 주문정보 노출 없이 편리하게 대량거래를 할 수 있을 것"이라고 기대했다.

다크풀(Dark Pool) 이란?

[이데일리 장영은 기자] 익명 거래 시장으로 기관투자자 전용 대량 매매 서비스를 말한다.

장 시작 전 기관 투자자로부터 매수·매도 주문을 받아 매칭하고 장 종료 후 거래를 체결하는 시스템이다. 이때 가격은 당일 거래량 가중평균 가격(VWAP)으로 계산된다.

다크풀을 이용하면 투자주체, 종목과 수량 등의 매매 정보가 장 종료 후 거래 체결을 보고하기 전까지 시장에 공개되지 않는다. 따라서 비밀스런 매매를 원하는 기관투자가들이 주로 이용한다.

전문가들은 다크풀의 장점으로 낮은 수수료와 빠른 거래 체결, 익명성 보장, 시장 가격에 영향을 미치지 않는다는 점을 들었다.

금융컨설팅 회사 탭그룹은 다크풀의 비중이 미국 주식 시장에서는 7% 정도이며 유럽에서는 전체의 4.1%를 차지한다고 보고 있다.

국내에서는 삼성증권이 지난해 다크풀 거래와 유사한 `코리아크로스`를 개설해 운영하고 있다. 오전 7시30분부터 한 시간 동안 국내외 기관 투자가에게 1억원 이상의 대량주문을 받아 매칭 작업을 하고, 오후 3시10분에 증권 거래소 대량매매 시스템(K-Blox)을 이용해 거래를 체결하는 방식이다.

장 시작 전 기관 투자자로부터 매수·매도 주문을 받아 매칭하고 장 종료 후 거래를 체결하는 시스템이다. 이때 가격은 당일 거래량 가중평균 가격(VWAP)으로 계산된다.

다크풀을 이용하면 투자주체, 종목과 수량 등의 매매 정보가 장 종료 후 거래 체결을 보고하기 전까지 시장에 공개되지 않는다. 따라서 비밀스런 매매를 원하는 기관투자가들이 주로 이용한다.

전문가들은 다크풀의 장점으로 낮은 수수료와 빠른 거래 체결, 익명성 보장, 시장 가격에 영향을 미치지 않는다는 점을 들었다.

금융컨설팅 회사 탭그룹은 다크풀의 비중이 미국 주식 시장에서는 7% 정도이며 유럽에서는 전체의 4.1%를 차지한다고 보고 있다.

국내에서는 삼성증권이 지난해 다크풀 거래와 유사한 `코리아크로스`를 개설해 운영하고 있다. 오전 7시30분부터 한 시간 동안 국내외 기관 투자가에게 1억원 이상의 대량주문을 받아 매칭 작업을 하고, 오후 3시10분에 증권 거래소 대량매매 시스템(K-Blox)을 이용해 거래를 체결하는 방식이다.

Buy Side vs. Sell Side

http://blog.naver.com/96scud/60047835415

Buy Side vs. Sell Side

From Columbia Business School COIN site

Buy Side vs. Sell Side

Lifestyle

The lifestyle on the buy side can vary depending on the fund's investment mandate (short-term trading, long only) and type of firm (hedge fund, mutual fund, insurance company). But generally speaking, the lifestyle is better than other industries (consulting and investment banking). The research analyst and portfolio manager hold market-driven hours and work weeks generally range from 55-70 hours per week.Work Environment

Most MBAs start out as research analysts covering a specific industry. They are usually the only person focusing on that industry, and the work is very independent from the other analysts. The work generally requires someone with a disciplined work ethic who does not need much supervision, but is able to stay motivated and be productive.From Columbia Business School COIN site

2010년 11월 20일 토요일

Algorithmic trading

http://en.wikipedia.org/wiki/Algorithmic_trading

In electronic financial markets, algorithmic trading or automated trading, also known as algo trading, black-box trading or robo trading, is the use of computer programs for entering trading orders with the computer algorithm deciding on aspects of the order such as the timing, price, or quantity of the order, or in many cases initiating the order without human intervention. Algorithmic Trading is widely used by pension funds, mutual funds, and other buy side (investor driven) institutional traders, to divide large trades into several smaller trades in order to manage market impact, and risk.[1][2] Sell side traders, such as market makers and some hedge funds, provide liquidity to the market, generating and executing orders automatically. A special class of algorithmic trading is "high-frequency trading" (HFT), in which computers make elaborate decisions to initiate orders based on information that is received electronically, before human traders are capable of processing the information they observe.

Algorithmic trading may be used in any investment strategy, including market making, inter-market spreading, arbitrage, or pure speculation (including trend following). The investment decision and implementation may be augmented at any stage with algorithmic support or may operate completely automatically ("on auto-pilot").

A third of all EU and US stock trades in 2006 were driven by automatic programs, or algorithms, according to Boston-based financial services industry research and consulting firm Aite Group.[3] As of 2009, high frequency trading firms account for 73% of all US equity trading volume.[4]

In 2006 at the London Stock Exchange, over 40% of all orders were entered by algo traders, with 60% predicted for 2007. American markets and european markets generally have a higher proportion of algo trades than other markets, and estimates for 2008 range as high as an 80% proportion in some markets. Foreign exchange markets also have active algo trading (about 25% of orders in 2006).[5] Futures and options markets are considered to be fairly easily integrated into algorithmic trading,[6] with about 20% of options volume expected to be computer generated by 2010.[7] Bond markets are moving toward more access to algorithmic traders.[8]

One of the main issues regarding high frequency trading is the difficulty in determining just how profitable it is. A report released in August 2009 by the TABB Group, a financial services industry research firm, estimated that the 300 securities firms and hedge funds that specialize in this type of trading took in roughly $21 billion in profits in 2008.[9]

Algorithmic and high frequency trading have been the subject of much public debate since the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission implicated them in the May 6, 2010 Flash Crash,[10][11][12][13][14][15][16][17] when the Dow Jones Industrial Average suffered its largest intraday point loss ever to that date, though prices quickly recovered.

See also

In electronic financial markets, algorithmic trading or automated trading, also known as algo trading, black-box trading or robo trading, is the use of computer programs for entering trading orders with the computer algorithm deciding on aspects of the order such as the timing, price, or quantity of the order, or in many cases initiating the order without human intervention. Algorithmic Trading is widely used by pension funds, mutual funds, and other buy side (investor driven) institutional traders, to divide large trades into several smaller trades in order to manage market impact, and risk.[1][2] Sell side traders, such as market makers and some hedge funds, provide liquidity to the market, generating and executing orders automatically. A special class of algorithmic trading is "high-frequency trading" (HFT), in which computers make elaborate decisions to initiate orders based on information that is received electronically, before human traders are capable of processing the information they observe.

Algorithmic trading may be used in any investment strategy, including market making, inter-market spreading, arbitrage, or pure speculation (including trend following). The investment decision and implementation may be augmented at any stage with algorithmic support or may operate completely automatically ("on auto-pilot").

A third of all EU and US stock trades in 2006 were driven by automatic programs, or algorithms, according to Boston-based financial services industry research and consulting firm Aite Group.[3] As of 2009, high frequency trading firms account for 73% of all US equity trading volume.[4]

In 2006 at the London Stock Exchange, over 40% of all orders were entered by algo traders, with 60% predicted for 2007. American markets and european markets generally have a higher proportion of algo trades than other markets, and estimates for 2008 range as high as an 80% proportion in some markets. Foreign exchange markets also have active algo trading (about 25% of orders in 2006).[5] Futures and options markets are considered to be fairly easily integrated into algorithmic trading,[6] with about 20% of options volume expected to be computer generated by 2010.[7] Bond markets are moving toward more access to algorithmic traders.[8]

One of the main issues regarding high frequency trading is the difficulty in determining just how profitable it is. A report released in August 2009 by the TABB Group, a financial services industry research firm, estimated that the 300 securities firms and hedge funds that specialize in this type of trading took in roughly $21 billion in profits in 2008.[9]

Algorithmic and high frequency trading have been the subject of much public debate since the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission implicated them in the May 6, 2010 Flash Crash,[10][11][12][13][14][15][16][17] when the Dow Jones Industrial Average suffered its largest intraday point loss ever to that date, though prices quickly recovered.

Contents[hide] |

- Outline of finance

- Alternative Trading Systems

- Artificial Intelligence

- Complex Event Processing

- Dark pools of liquidity

- Electronic Communication Network

- Electronic trading

- Electronic trading platform

- Implementation shortfall

- Investment strategy

- Quantitative trading

- Execution Management System

- Flash Crash

- High-frequency trading

Implementation shortfall

In financial markets, Implementation Shortfall is the difference between the decision price and the final execution price (including commissions, taxes, etc.) for a trade. This is also known as the "slippage". Agency trading is largely concerned with minimizing implementation shortfall and finding liquidity.

TCA

http://www.auditmypc.com/acronym/tca.asp

TCA – Transaction Cost Analysis

There may be many popular meanings for TCA with the most popular definition being that of Transaction Cost Analysis

http://www.streambase.com/trans-cost-analysis.htm

Financial markets are inherently volatile, characterized by shifting values, risks and opportunities. The prices of individual securities are frequently changing for numerous reasons, including shifts in perceived value, localized supply/demand imbalances, and price changes in other sector investments or the market as a whole. Reduced liquidity adds price volatility and market risk to any contemplated transaction, and in the face of this volatility, Transaction Cost Analysis (TCA) has become increasingly important to help firms measure how effectively both perceived and actual portfolio orders are completed.

TCA – Transaction Cost Analysis

There may be many popular meanings for TCA with the most popular definition being that of Transaction Cost Analysis

http://www.streambase.com/trans-cost-analysis.htm

Financial markets are inherently volatile, characterized by shifting values, risks and opportunities. The prices of individual securities are frequently changing for numerous reasons, including shifts in perceived value, localized supply/demand imbalances, and price changes in other sector investments or the market as a whole. Reduced liquidity adds price volatility and market risk to any contemplated transaction, and in the face of this volatility, Transaction Cost Analysis (TCA) has become increasingly important to help firms measure how effectively both perceived and actual portfolio orders are completed.

Conceptually, TCA represents the difference between two amounts, and StreamBase’s Event Processing Platform can play an active role in computing TCA in real-time. The first amount represents the amount if the transaction was instantaneously executed at the price prevailing when the portfolio manager made the decision, without any additional costs. The second amount represents what would have been or actually was realized. This second amount includes direct costs, such as commissions, settlement costs and taxes, as well as indirect costs from timing delays, market impact and missed opportunities. The difference between these two amounts is often referred to as transaction "slippage".

Increased slippage amounts directly reduce investor returns and hurt relative performance versus the performance of competing investment managers. In an environment of increased regulatory scrutiny, fierce competition, and relatively low returns on equities, TCA has become a staple at buy-side firms to analyze the efficiency of their entire investment processes.

If an entire stock order is sold at once, the resulting sale price generally will be locally depressed relative to the portfolio manager's decision price. This is due to the trade-off between time and price, even with stocks that have the best market liquidity. Alternatively, if the order is distributed into the market over time, there is an opportunity cost that the market price might decline over time. What’s more, timing delays between the portfolio manager, compliance officials, traders and actual delivery of the order to the market contribute to overall opportunity cost.

Implementation Shortfall (IS) algorithms implemented in StreamBase measure and balance the risk of moving the security price against the urgency of filling the order. Multiple security IS versions use advanced quantitative techniques to continually calculate the optimal execution, attempting to minimize liquidity impact, opportunity costs, market risk and information dissemination across the entire portfolio.

With technologies such as StreamBase’s Event Processing Platform, the graphical development paradigm enables rapid implementation of trade execution strategies, and easy adjustment of these strategies on the fly to reflect changing market conditions. The high performance server captures more refined data, and the low latency processing platform enables real-time TCA to help pinpoint exactly where and when costs occur in open orders and completed transactions. Process bottlenecks can then be identified more frequently and resolved more efficiently. And the extensive library of pre-built adapters to market data feeds, historical data, and interactive dashboards also provides smoother integration with even the most complex environments. The net result is real-time TCA that enables investment ideas to be more efficiently implemented while minimizing slippage costs.

One of the top three EU hedge funds, with more than €7B in assets under management, built a real-time pre-trade analysis application using StreamBase. This application identified best execution strategies, reduced slippage, and monitored and evaluated broker performance using precise real-time and historical data. By processing more than double the amount of market data than was possible with the previous infrastructure, the firm is now dramatically reducing execution costs and increasing trading profits.

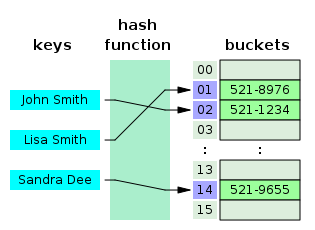

Hash table

http://en.wikipedia.org/wiki/Hash_table

"Post Office!!"

"Unordered map" redirects here. For the proposed C++ class, see unordered_map (C++).

In computer science, a hash table or hash map is a data structure that uses a hash function to map identifying values, known as keys (e.g., a person's name), to their associated values (e.g., their telephone number). Thus, a hash table implements an associative array. The hash function is used to transform the key into the index (the hash) of an array element (the slot or bucket) where the corresponding value is to be sought.

Ideally, the hash function should map each possible key to a unique slot index, but this ideal is rarely achievable in practice (unless the hash keys are fixed; i.e. new entries are never added to the table after creation). Most hash table designs assume that hash collisions—the situation where different keys happen to have the same hash value—are normal occurrences and must be accommodated in some way.

In a well-dimensioned hash table, the average cost (number of instructions) for each lookup is independent of the number of elements stored in the table. Many hash table designs also allow arbitrary insertions and deletions of key-value pairs, at constant average (indeed, amortized[1]) cost per operation.[2][3]

In many situations, hash tables turn out to be more efficient than search trees or any other table lookup structure. For this reason, they are widely used in many kinds of computer software, particularly for associative arrays, database indexing, caches, and sets.

Hash tables should not be confused with the hash lists and hash trees used in cryptography and data transmission.

A small phone book as a hash table.

"Post Office!!"

"Unordered map" redirects here. For the proposed C++ class, see unordered_map (C++).

In computer science, a hash table or hash map is a data structure that uses a hash function to map identifying values, known as keys (e.g., a person's name), to their associated values (e.g., their telephone number). Thus, a hash table implements an associative array. The hash function is used to transform the key into the index (the hash) of an array element (the slot or bucket) where the corresponding value is to be sought.

Ideally, the hash function should map each possible key to a unique slot index, but this ideal is rarely achievable in practice (unless the hash keys are fixed; i.e. new entries are never added to the table after creation). Most hash table designs assume that hash collisions—the situation where different keys happen to have the same hash value—are normal occurrences and must be accommodated in some way.

In a well-dimensioned hash table, the average cost (number of instructions) for each lookup is independent of the number of elements stored in the table. Many hash table designs also allow arbitrary insertions and deletions of key-value pairs, at constant average (indeed, amortized[1]) cost per operation.[2][3]

In many situations, hash tables turn out to be more efficient than search trees or any other table lookup structure. For this reason, they are widely used in many kinds of computer software, particularly for associative arrays, database indexing, caches, and sets.

Hash tables should not be confused with the hash lists and hash trees used in cryptography and data transmission.

A small phone book as a hash table.

Contents

[hide]2010년 11월 19일 금요일

B-tree

http://en.wikipedia.org/wiki/B-tree

Not to be confused with Binary tree.

In computer science, a B-tree is a tree data structure that keeps data sorted and allows searches, sequential access, insertions, and deletions in logarithmic amortized time. The B-tree is a generalization of a binary search tree in that a node can have more than two children. (Comer, p. 123) Unlike self-balancing binary search trees, the B-tree is optimized for systems that read and write large blocks of data. It is commonly used in databases and filesystems.

Not to be confused with Binary tree.

In computer science, a B-tree is a tree data structure that keeps data sorted and allows searches, sequential access, insertions, and deletions in logarithmic amortized time. The B-tree is a generalization of a binary search tree in that a node can have more than two children. (Comer, p. 123) Unlike self-balancing binary search trees, the B-tree is optimized for systems that read and write large blocks of data. It is commonly used in databases and filesystems.

Contents

[hide]- 1 Overview

- 2 The database problem

- 3 Technical description

- 4 Best case and worst case heights

- 5 Algorithms

- 6 B-trees in filesystems

- 7 Variations

- 8 See also

- 9 Notes

- 10 References

- 11 External links

| B-tree | ||

|---|---|---|

| Type | Tree | |

| Invented | 1972 | |

| Invented by | Rudolf Bayer, Edward M. McCreight | |

| Time complexity in big O notation | ||

| Average | Worst case | |

| Space | ||

| Search | O(log n) | O(log n) |

| Insert | O(log n) | O(log n) |

| Delete | O(log n) | O(log n) |

In-memory database

http://en.wikipedia.org/wiki/In-memory_database

An in-memory database (IMDB; also main memory database system or MMDB) is a database management system that primarily relies on main memory for computer data storage. It is contrasted with database management systems which employ a disk storage mechanism. Main memory databases are faster than disk-optimized databases since the internal optimization algorithms are simpler and execute fewer CPU instructions. Accessing data in memory provides faster and more predictable performance than disk. In applications where response time is critical, such as telecommunications network equipment, main memory databases are often used.[1]

An in-memory database (IMDB; also main memory database system or MMDB) is a database management system that primarily relies on main memory for computer data storage. It is contrasted with database management systems which employ a disk storage mechanism. Main memory databases are faster than disk-optimized databases since the internal optimization algorithms are simpler and execute fewer CPU instructions. Accessing data in memory provides faster and more predictable performance than disk. In applications where response time is critical, such as telecommunications network equipment, main memory databases are often used.[1]

Contents

[hide]- 1 ACID support

- 2 "Hybrid" in-memory/on-disk databases

- 3 Commercial products

- 4 Products

- 5 References

- 6 See also

- 7 External links

Message-Oriented Middleware

http://en.wikipedia.org/wiki/Message-oriented_middleware

Message-oriented middleware (MOM) is software infrastructure focused on sending and receiving messages between distributed systems. MOM allows application modules to be distributed over heterogeneous platforms, and reduces the complexity of developing applications that span multiple operating systems and network protocols by insulating the application developer from the details of the various operating system and network interfaces. APIs that extend across diverse platforms and networks are typically provided by MOM.[citation needed]

MOM is a software that resides in both portions of client/server architecture and typically supports asynchronous calls between the client and server applications. MOM reduces the involvement of application developers with the complexity of the master-slave nature of the client/server mechanism.

Message-oriented middleware (MOM) is software infrastructure focused on sending and receiving messages between distributed systems. MOM allows application modules to be distributed over heterogeneous platforms, and reduces the complexity of developing applications that span multiple operating systems and network protocols by insulating the application developer from the details of the various operating system and network interfaces. APIs that extend across diverse platforms and networks are typically provided by MOM.[citation needed]

MOM is a software that resides in both portions of client/server architecture and typically supports asynchronous calls between the client and server applications. MOM reduces the involvement of application developers with the complexity of the master-slave nature of the client/server mechanism.

Contents

[hide]2010년 11월 14일 일요일

http://www.swift.com/

http://www.swift.com/

SWIFT is the Society for Worldwide Interbank Financial Telecommunication, a member-owned cooperative through which the financial world conducts its business operations with speed, certainty and confidence. More than 9,000 banking organisations, securities institutions and corporate customers in 209 countries trust us every day to exchange millions of standardised financial messages.

Our role is two-fold. We provide the proprietary communications platform, products and services that allow our customers to connect and exchange financial information securely and reliably. We also act as the catalyst that brings the financial community together to work collaboratively to shape market practice, define standards and consider solutions to issues of mutual interest.

SWIFT enables its customers to automate and standardise financial transactions, thereby lowering costs, reducing operational risk and eliminating inefficiencies from their operations. By using SWIFT customers can also create new business opportunities and revenue streams.

SWIFT has its headquarters in Belgium and has offices in the world's major financial centres and developing markets. SWIFT provides additional products and associated services through Arkelis N.V., a wholly owned subsidiary of SWIFT, the assets of which were acquired from SunGard in 2010.

SWIFT is solely a carrier of messages. It does not hold funds nor does it manage accounts on behalf of customers, nor does it store financial information on an on-going basis. As a data carrier, SWIFT transports messages between two financial institutions. This activity involves the secure exchange of proprietary data while ensuring its confidentiality and integrity.

SWIFT for securities market infrastructures

SWIFT is the Society for Worldwide Interbank Financial Telecommunication, a member-owned cooperative through which the financial world conducts its business operations with speed, certainty and confidence. More than 9,000 banking organisations, securities institutions and corporate customers in 209 countries trust us every day to exchange millions of standardised financial messages.

Our role is two-fold. We provide the proprietary communications platform, products and services that allow our customers to connect and exchange financial information securely and reliably. We also act as the catalyst that brings the financial community together to work collaboratively to shape market practice, define standards and consider solutions to issues of mutual interest.

SWIFT enables its customers to automate and standardise financial transactions, thereby lowering costs, reducing operational risk and eliminating inefficiencies from their operations. By using SWIFT customers can also create new business opportunities and revenue streams.

SWIFT has its headquarters in Belgium and has offices in the world's major financial centres and developing markets. SWIFT provides additional products and associated services through Arkelis N.V., a wholly owned subsidiary of SWIFT, the assets of which were acquired from SunGard in 2010.

SWIFT is solely a carrier of messages. It does not hold funds nor does it manage accounts on behalf of customers, nor does it store financial information on an on-going basis. As a data carrier, SWIFT transports messages between two financial institutions. This activity involves the secure exchange of proprietary data while ensuring its confidentiality and integrity.

SWIFT for securities market infrastructures

2010년 11월 12일 금요일

anti-algorithmic trading

Anti-Algorithmic Trading

from the International Association of Risk and Compliance Professionals (IARCP)

I am a mathematician, so I am supposed to like algorithms. I love them. But not always.

I love algorithms that are used by traders in algorithmic trading. I don't believe in algorithms that replace humans in decision making. That buy and sell without human intervention. Yes, these algorithms can be useful, but they can also be very dangerous.

I do understand that algorithms and automated systems can be very quick and effective. For example, I like smart order routing algorithms, like “Guerrilla”, the algorithm developed by Credit Suisse that slices big orders into smaller unobtrusive sizes. Great algorithm, very effective.

I like “Sniper”, also developed by Credit Suisse, that detects dark pools of liquidity (hidden sources of liquidity that are not shown on conventional trading platforms provided by the stock exchanges). I like “Benchmark” algorithms that achieve a specific benchmark.

The problem is that we take algorithmic trading far too seriously, we rely on it, and we run the risk of transforming it from a useful tool to a weapon of mass destruction (WMD). Why? All these algorithms trade according to well known or predictable rules and can be used against the free market or the firms that rely on them. This is a disaster waiting to happen.

Traders do not really understand information security, deception management, information systems. I have never met them in Black Hut conference in Las Vegas. They have learned Euclidean geometry, and they strongly believe that "A Straight Line Is the Shortest Distance between Two Points". Not always, and definitely not in information security. A Straight Line is the most obvious and most predictable route, and this knowledge can be used against us.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Anti-Algorithmic Trading

Algorithmic trading is the use of computer systems, programs and advanced mathematical models for entering trading orders. Algorithms, not humans decide on aspects such as the timing, price and the quantity of orders.

Some algorithms initiate orders based on information received electronically, understood by the algorithms only. On the positive side, they are quick, so they can exploit opportunities (arbitrage, statistical arbitrage, trend following). I like statistical arbitrage, and I remember that I liked some algorithmic trading systems that really helped, but these days there are so many sophisticated systems and algorithms competing to exploit the same opportunities, that we have to find something more creative.

On the negative side, more and more trades are driven by automatic programs, and algorithms replace traders. At the London Stock Exchange for example, over 50% of all orders were entered by algo traders. American markets have an even higher proportion of algo trades (estimates range as high as 80% proportion in some markets).

Electronic platforms were supposed to execute simple trades, and leave hedge fund managers or traders at the financial firms and brokerages free to come up with new ideas for making money. These days electronic platforms tend to execute all trades, and leave humans free to find another job. Which one? Technical staff, as more and more firms have more people working in their technology area than people on the trading desk.

Computers not only learn what is new from firms such as Reuters, Dow Jones, Bloomberg and Thomson Financial, but also decide if the news is good or bad so that automated trading can work directly on the news stories. “There is a real interest in moving the process of interpreting news from the humans to the machines” said Kiristi Suutani, global business manager of algorithmic trading at Reuters.

Jobs once done by human traders are being switched to computers. Every day we read about the speed and the processing power of computers and networks, and their ability for “lightning-quick trades”. When we read success stories about humans, like hedge fund managers, we also read about their high management and performance fee. We rarely speak about the cost of the systems that replace humans (tens of billions).

I do not like certain algorithms called “sniffers”, that sniff out algorithmic trading by others and the algorithms being used by them. They can “game” the system, and may trigger buy orders to generate a better market price into which to sell. These algorithms can be very dangerous. We move towards Information Operations and Information Warfare-like environment.

Information is no longer a staff function but an operational one. It is deadly as well as useful.

--- Executive Summary, Air Force 2025 report

No, I am not kidding. Information Operations is the integrated employment of the core capabilities of electronic warfare, computer network operations, psychological operations, military deception and operations security, in concert with specified supporting and related capabilities, to influence, disrupt, corrupt or usurp adversarial human and automated decision making while protecting our own.

The above definition of Information Operations should have nothing to do with trading. But it has. If you read the definition carefully, you will see that trading is very similar to war, and information is always a weapon.

Hedge funds and financial organizations of both, the buy side and the sell side, must remember that computers should help humans, not make decisions. Traders must not forget that they are not IT or Information Security experts, and that mathematicians are usually not born for risk management. So many firms rely on systems they do not understand.

No, these risks are not covered by your risk models. They are 15 standard deviations from the mean (nowhere). They are High Impact / Low Likelihood events, hidden under the "fat tail" of the distribution.

Systems should help humans, not replace them.I really like strategies and approaches that can not be programmed into systems. Creative, non-formulaic, anti-algorithmic.

Note

This web site does not constitute or offer legal, financial or other advice upon which you may act or rely. Specific professional advice should be taken in respect of any individual matter.

George Lekatis

General Manager and Chief Compliance Consultant

Compliance LLCAmazon.com Widgets

2010년 11월 11일 목요일

한국에서 HFT는 가능할까, 불가능할까?

by Smith Kim on Thursday, November 11, 2010 at 1:36pm

1.

알고리즘트레이딩.고빈도트레이딩(High Frequency Trading). 인구에 회자하고 있습니다. 금융투자회사도 같은 듯 다른 이유로 관심을 가지고 있습니다. 몇 일전 어떤 분과 HFT에 대핸 트위터로 이야기할 기회가 있었습니다. 요지는 이렇습니다.

"한국과 아시아에서 HFT는 유의미한 전략이 아니다. 한국에 의미없는 HFT를 소개하고 도입하자고 하는 취지가 이해하기 어렵다"

같은 날 얼굴을 보고 제가 생각하는 바를 설명했죠. 또한 상대방이 말하고자 하는 바를 이해했습니다.그러면서 들었던 생각입니다.

"분명 HFT나 알고리즘트레이딩이라는 단어를 같이 사용하고 있는데 서로 의미하는 바나 사용하는 맥락이 다르구나!!"

그래서 최소한 서로가 대화를 할 때 같은 의미로 사용하자는 취지에서 정리해보았습니다.

2.

우선 증권사에서 펴낸 자료를 따라가면서 알아보도록 하겠습니다. 좀 멀리서 시작해보도록 하죠. Algo Trading이든 HFT이든 기계가 의사결정을 한다는 면에선 시스템트레이딩입니다.시스템트레이딩을 2007년쯤 대신증권에서 정리하였습니다.

위 글에서는 알고리즘 트레이딩을 아래와 같이 정의하고 있습니다.

최근에는 알고리즘 트레이딩(Algorithm Trading)이란 용어의 시스템 트레이딩 방법이 많이 사용되고 있다. 알고리즘 트레이딩이란 자동 주문 시스템이란 의미와 알파(alpha) 수익률 창출을 위한 차익거래 매매의 의미를 내포한 매매형태로서, 대량 주문을 자동으로, 동시 주 문을 자동으로, 분할 주문을 자동으로 설정하는 형태가 많이 사용된다. 주로 기관 투자가가 많이 사용하고 있으며 시스템 매매의 한 분류로 볼 수 있다.

이제 본격적으로 알고리즘트레이딩과 HFT를 어떻게 정의하는지 알아보도록 하겠습니다. 구글링을 해보니까 우리투자증권외 자료를 구하지 못했습니다.

위 글에서는 알고리즘 트레이딩을 다음과 같이 정의합니다.사실 이 정의는 정의로써 문제가 있습니다. 알고리즘트레이딩을 정의하면서 '알고리즘에 의거한"이라는 동어반복을 했기때문입니다.(^^)

알고리즘에 의거한 자동화된 매매를 의미함. 자동화 매매를 이용하는 이유는 거래대상의 가격과 시장 상황 등을 유기 적으로 분석해 해당 알고리즘에 의거한 매매를 최소의 거래비용을 통해 구현하기 위함임. 기본 개념만 놓고 보면 프로그램매매와 매우 유사하며 High Frequency Trading도 알고리즘 트레이딩의 일종으로 볼 수 있음

다음으로 HFT에 대한 정의입니다. 아래글을 유심히 읽어보았지만 HFT에 대한 정의가 매우 막연합니다. 아주 단순화하면 단위시간당 주문건수가 무지무지하게 많다는 정도로 정의하고 있습니다.

High Frequency Trading(이하 HFT)이란 상당히 빈번하게 발생하는 형태의 매매를 의미한다. 컴퓨터 프로그램을 이용한 트레이딩 기법의 일종으로 컴퓨터 성능의 향상과 자동화 기술 의 발달로 가능하게 된 새로운 트레이딩의 형태로 정의 내릴 수 있다.

마지막으로 한국거래소는 어떻게 정의하는지 알아보도록 하겠습니다. 시장감시위원회에서 펴낸 알고리즘트레이딩관련 가이드라인입니다.

위의 가이드라인에서는 다음과 같은 의미로 알고리즘트레이딩을 사용합니다.

알고리즘 트레이딩은 사전에 설정된 매개변수 및 제약조건에 기초해 주문시간과 수량을 자동으로 생성하는 알고리즘을 통해 실행되는 주문 및 거래체계

마찬가지로 시장감시위원회는 HFT를 다음과 같이 정의합니다.

HFT는 IT기술 발달을 기반으로 고도의 프로그램을 통해 수만건의 거래를 일순간에 처리하는 방법으로 초단기간에 호가 상황을 파악하여 주문을 제출하거나 취소하여 초단기이익을 얻는 알고리즘거래의 일환으로 슈퍼컴퓨터를 이용한 알고리즘 트레이딩 기반의 초단기 매매기법

이상이 한국에서 알고리즘트레이딩이나 HFT를 다룬 글의 전부는 아니지만 거래소, 증권회사등의 정의를 살펴보았습니다.

3.

이제 알고리즘트레이딩과 HFT를 어떤 의미로 정의하여야 할까요? 우선 알고리즘트레이딩은 비슷한 내용으로 정리될 듯 합니다.제가 지금까지 본 정의중 2005년에 한 글에서 정리한 아래 문장이 가장 마음에 듭니다.

Algorithmic trading is defined as “placing a buy or sell order of a defined quantity into a quantitative model that automatically generates the timing of orders and the size of orders based on goals specified by the parameters and constraints of the algorithm.

이 말을 우리말로 번역하면 거래소에서 내린 정의와 별반 다르지 않습니다.

알고리즘 트레이딩이란 사전에 설정된 매개변수 및 제약조건에 기초해 주문시간과 수량을 자동으로 생성하는 정략적인 모델(수학적 모델)을 통해 실행되는 주문 및 거래체계

문제는 HFT(High Frequency Trading)입니다. 어떤 분은 '거래횟수'를 강조하는 분도 있고 어떤 분은 '전략 혹은 알고리즘'을 강조하는 분도 계십니다.미국도 명확히 HFT가 무엇인지에 대해 의견이 통일되어 있지 않습니다.

HFT를 140자 이내로 정의하면 - Flash Crash 보고서이후

그렇지만 High Frequency Trading은 1)알고리즘트레이딩이라는 매매기법의 발전 2)HPC(Low Latency등 포함)와 같은 기술적인 진보를 배경으로 하고 있다는 점을 명확히 하여야 합니다.

이를 전제로 HFT를 정의하면

HPC와 Low Latency기술을 기반으로 시장내 유동성의 불균형과 가격의 비효율성으로부터 이익을 얻기 위하여 실시간 호가상황을 판단하여 아주 짧은 시간동안 다량의 주문을 내고 아주 작은 이익을 내는 자동화된 매매전략들

이 아닐까 합니다.

High-frequency trading involves the large-scale turnover of numerous positions, making a small return on each turnover 와

Define high frequency as fully automated trading strategies that seek to benefit from market liquidity imbalances or other short-term pricing inefficiencies. And that goes across asset classes, extending from equities and derivatives into currencies and a little into fixed income을 덧붙인 정의

Breaking it Down: An Overview of High-Frequency Trading중에서

4.

그러면 한국에서 HFT의 가능성을? 먼저 High Frequency라는 말에 연연하지 않았으면 합니다. 무엇이 많다는 기준은 나라마다 시장구조가 다르기때문에 다르다고 생각합니다. KRX관계자가 이런 말을 했습니다.

국내의 경우 단일거래소 체제 및 회원사 시스템을 통한 호가입력방식의 제한으로 알고리즘 트레이딩 등 신매매기법이 활성화되기는 어려울 것이지만 앞으로 이와 관련한 불공정거래 발생 가능성에 대비하겠다

알고리즘 트레이딩등 新매매기법 해외서 활성화중에서

만약 미국처럼 시장이 여러개의 거래소로 나눠졌고 각 거래소간의 가격차이로 부터 기회를 발견하고 코로케이션서비스등으로 Low Latency를 구현하고 막대한 돈을 IT에 투자하는 상황과 비교하면, 한국은 무엇이든 불가능합니다. 그렇지만 Low든 High든 상대적인 개념입니다. KRX의 시장 참여자들을 놓고 비교함이 타당합니다. 하루에 100번 거래를 하고 주문속도가 10ms이하인 상황에서 ELW를 매매하는 슈퍼메뚜기들이 초당 몇 천번, 주문속도가 100마이크로초를 다투는 미국 HFT와 비교하면 HFT가 아니지만 한국내 다른 참여자와 비교하면 HFT라고 할 수 있습니다.

흔히들 HFT를 말할 때 전략이라고 말하는 것들이 있습니다.앞서 우리투자증권의 자료는 다음을 HFT전략이라고 합니다.

1.Flash Orders

2.Liquidity Rebate Trading

3.Market Making

4.Dark Pool Trading

위에서 자료를 소개한 Overview Of HFT를 보면 다음과 같은 전략을 HFT전략이라고 합니다.

1.Market Making

2.Statistical Arbitrage

3.Low Latency Trading

4.Liquidity Detection

5.Flash Orders

Breaking it Down: An Overview of High-Frequency Trading에서는 다음과 같은 전략이라고 합니다.

With arbitrage strategies, Iati explains, traders look to correlate prices between securities in some way and trade off of the imbalances in those correlations. "Those imbalances can and do occur in microsecond time frames," he comments. "The more time that elapses, the more time for those imbalances to be corrected. A trader who can achieve [just] a millisecond of latency can capture some of that opportunity."

Pairs trading, and more specifically cross-asset pairs trading, also is a popular high-frequency trading strategy, according to Iati. "For example, if I am looking at a correlation between Coke and Pepsi -- if one moves up one would expect the other to move up," explains Iati. "Or, in the case of cross-asset pairs, the correlation between the derivative and an underlying asset. So the price of each is tied together. High-frequency traders continuously calculate the value of both, looking for an imbalance."

Another high-frequency strategy is volatility trading or trading on relative price movement rather than absolute price movement. In this case, Iati says, "Traders make money on volatility, not necessarily on movement."

A fourth high-frequency strategy is short-term statistical arbitrage, or a complex form of pairs trading that involves trading a broad range of securities that are correlated, Iati explains. "Stat arb has traditionally been long term, but over the last couple of years that has evolved and it has moved into shorter time frames," says Iati. "Those strategies have been adjusted to take advantage of shorter time horizons, minimizing capital at risk."

The last -- and most controversial -- type of high-frequency trading, according to Iati, is "liquidity detection." "This is when firms are looking to decipher whether there are large orders existing in a matching engine by sending out small orders, or pinging to look for where large orders might be resting," he relates. "When a small order is filled quickly, there is likely to be" a large order behind it.

위의 전략중 Flash Order와 같이 미국 시장구조에 특화된 전략도 있습니다. 반면 Latency Arbitrage와 같이 어느 나라 시장에서도 적용할 수 있는 전략도 있습니다. 슈퍼메뚜기든 ITG와 같은 회사든 상대적으로 많은 거래횟수와 상대적으로 낮은 지연시간(Low Latency)를 이용하여 매매를 한다고 하면 그게 바로 HFT전략이라는 생각입니다.

橘化爲枳(귤화위지).귤이 회수를 건너면 탱자가 된다는 말처럼 미국이나 유럽의 HFT가 물 건너 한국에 와서 한국형 HFT가 되는 것과 같습니다. 이를 테면 Orange(오륀지)가 한국에서 Orange(오렌지)로 된 것처럼(^^)

5.

이제 HFT든 알고리즘 트레이딩이든 확대된다고 예상을 하면 어디에서 출발하여야 할까요? 저는 우선 두가지가 필요하다고 생각합니다.

첫째는 알고리즘개발이나 전략 수립에 필수적인 백테스팅환경을 구축하는 일입니다. 많은 프랍데스크나 부티크는 종가기준으로 모델링하는 듯 합니다. 그렇지만 HFT와 같은 트레이딩은 틱데이타(Tick Based Data)를 기준으로 모델링하여야 합니다.미국 NYSE같은 경우 테라단위 데이타입니다. 몇 년단위의 데이타인지에 따라 다르지만 한국시장은 몇백기가정도가 되지 않을까 합니다. 이런 데이타를 관리하고 분석할 수 있는 데이타관리방안 및 시스템이 구축되어야 합니다.

둘째는 Low Latency환경 구축입니다. Low Latency 혹은 Speed가 트레이딩에 어떤 의미가 있을까요? 차익트레이딩과 펀더멘탈트레이딩은 Low Latency에 대해 다른 의미가 있다고 합니다. 차익트레이딩은 가격정보에 촛점을 두고 순간적으로 발생하는 기회를 포착하는데 목표를 두고 있습니다. 시장에 발 빠르게 대응할 수 있는 환경이 중요합니다. 반면 펀터멘탈트레이딩은 시장에 미치는 영향과 비용을 줄이면서 기회를 포착하는 방식입니다.

Arbitrage driven trading is focused on market data and information. Complex quantitative models are designed to capture temporary opportunities in the marketplace. This trading technique is specifically designed to capture alpha, which can erode within milliseconds. In many cases these models have optimised everything in terms of throughput capacity and the ability to react to changes in information and trading opportunities. At this point of parity, the trader will be left with basic physics – he will have to turn to faster response times rather than changes in information for alpha capture. As latency increases with distance, locating trading technology close to the market centre is the obvious next step in minimising alpha erosion. And at what point does distance make a significant impact in terms of latency? An additional source of arbitrage may be targeting the trading venue itself – by trading the faster venue in order to optimise the relative differences in speeds.

Fundamental trading is opportunistic – unlike the arbitrage-driven trader, the fundamental trader’s main concern is about participating in a fragmented market while minimising impact and delay cost. Most orders are duration orders which may potentially be on the order books right the way through to market close. Alpha erosion over the course of the day is of more importance than split second speed. While latency is not of primary concern, speed is still a key component of best execution and ensuring the capture of liquidity at the best available prices. Venues that enable anonymous trading are becoming more of a feature in this environment, and can be seen in the recent proliferation and popularity of dark liquidity pools. In order to meet their trading objectives, fundamental traders require a solid understanding of order placement methodologies and their broker’s infrastructure and technology.

Check your speed중에서

그런데 미국의 경우 HFT와 펀터멘탈트레이딩의 융합하는 방향으로 나아가야 한다는 의견도 있습니다.

But he argues that to reignite interest in fundamentally driven trading, money managers will have to significantly change the ways they operate – and one way could be to merge HFT and fundamental strategies.

“The current US market structure basically features three types of players. First, the indexers, who allocate capital to passive indices such as the S&P 500. Second, active managers, who employ fundamental analysis. Then HFT, which dominates volumes but acts more like a marketmaker than investor.

“There is nothing, apart from pre-existing policies, to stop fundamental managers incorporating HFT techniques into their own approaches to investment.

“Better returns through creativity are a hallmark of capital markets. Traditional managers will have to adapt, as it is hard to see how the economic backdrop will change any time soon.”

Money managers have to change strategies중에서

어찌되었든 트레이딩에서 Low Latency가 점점더 중요해진다고 사실은 변함이 없습니다. 이미 국내에서도 Latency를 둘러싼 경쟁이 시작되었습니다. KRX가 어떤 정책을 정하든 Low Latency가 증권사의 핵심경쟁력중 하나가 될 것입니다.

6.

마지막으로 KRX의 정책을 보도록 하겠습니다. 금융당국과 KRX는 서로 다른 목표를 지향합니다.금융당국은 투명성,공정성을 지향합니다. KRX는 시장의 성장을 목표로 합니다. 물론 겹치는 부분이 있습니다.

알고리즘트레이딩이나 HFT에 대한 KRX는 규제와 도입사이에서 갈팡질팡 하는 듯 합니다. 우선 KRX 시장감시위원회에서는 체결단위가 아니라 호가단위로 수수료를 부과하는 방안을 도입하겠다고 합니다. 규제책입니다.

투자자들을 현혹하고 전산장애 등을 일으키는 허수성 호가 매매를 막기 위해 ‘체결’에 따라 수수료를 물게 하는 현재의 방식을 ‘호가’에 따라 수수료를 부과하는 미국 방식으로 바꾸는 방안도 함께 검토할 계획이다.

이 철환(55) 한국거래소 시장감시위원장은 지난 5일 서울신문과 가진 인터뷰에서 이렇게 밝히고 “미국, 유럽에서 널리 이뤄지고 있는 컴퓨터 알고리즘 거래가 합리적으로 발전하기 위해서는 호가에 수수료를 붙이는 방식으로 이용자들이 비용을 부담하는 게 맞다고 본다.”고 말했다. 경제관료에서 주식시장의 불공정 거래를 잡아내는 시장감시위원장으로 옮긴 지 3년째를 맞은 그는 요즘 마냥 규제할 수도, 마냥 풀어줄 수도 없는 알고리즘 거래의 균형점을 찾는 데 고심하고 있다고 했다.

“폐단 많은 극초단타 매매 하루 주문수량 제한 검토” 중에서

반대로 시중에 공개하지 않고 언론사 기사들에게 제공한 보고서는 허용이라는 입장을 보여줍니다. 아래 글중에 '해외 신매매기법 현황 및 시사점'라는 자료를 찾으려고 노력했지만 기사도 없다고 하네요.(^^;)

그런데 지난 23일, 거래소는 '해외 신매매기법 현황 및 시사점'이라는 자료를 통해 "해외거래소의 경우 알고리즘 거래, 고주파매매를 규제하기보다 오히려 장려하는 상황"이라고 태도를 바꿨다. "특히 HFT는 현재 불공정 관련 문제점이 없다"고 아예 단정지었다.신종 IT기술을 동원한 거래기법 도입을 주시하고 지속적으로 감시하겠다던 거래소가 '감시'보다는 '장려'쪽으로 돌아선 것이다.

한국거래소의 수익마인드중에서

아래에서도 '알고리즘 매매 수용을 위한 시장관리 방안'이라는 보고서가 나옵니다만 확인이 불가능합니다.

우리나라 거래소는 어떤가. SEC의 규제 논의가 벌써 작년 9월에 시작되었는데도 거래소는 1년이 지난 10월에야 태스크포스를 가동했다. 그 사이 국내 한 증권사는 외국인 기관투자가를 대상으로 극초단타 매매 서비스를 시작했다. 국감장에서 방지 대책을 제대로 수립하지 못하고 있다는 질타를 받기도 했다.

대책을 마련하겠다는 거래소는 기자에게 '알고리즘 매매 수용을 위한 시장관리 방안'이라는 보고서를 보내왔다. 극초단타 매매를 포함하는 알고리즘 매매를 피할 수 없는 세계적인 조류로 판단하고 있었다. 물론 알고리즘 매매와 관련한 규제 강화 내용도 담겨 있다. 그러나 '수용'을 전제로 한 보고서의 진정성에 대해서는 의문이 여전히 남을 수밖에 없다.

극초단타매매와 한국의 현실중에서

KRX가 샌드위치가 된 듯 합니다. 규제를 바라는 감독당국와 허용을 바라는 업계의 요구사이에서 갈팡질팡하는 듯 합니다.

이런 글이 기억납니다. 미국 투자은행은 볼커룰로 돈줄인 프랍트레이딩을 할 수 업게 되었습니다. 또한 여러가지로 규제가 많아서 예전처럼 운용할 수 없다고 합니다. 그래서 지하(Going undergroud)로 숨는다고 합니다. 한국으로 말하자만 사설 헤지펀드나 사모펀드같은 식으로 간다고 합니다.

시장에 이익을 보려는 사람은 무슨 수를 쓰더라도 방법을 찾습니다. 막는다고 막히진 않습니다.

7.

이 글을 보다 몰랐던 사실을 알았습니다. 이전에 KRX 시장감시위원회에서 펴낸 자료에서 짐작은 했지만 공문으로 내려보낸 줄을 몰랐습니다. 그래서 위에 PDF로 변화하여 올려놓았습니다.

지 난 5월 18일 KRX는 공문을 통해 알고리즘 트레이딩과 관련한 가이드라인을 제시했다. 알 고리즘 트레이딩 과정에서 발생하는 허수성 호가 및 가장성 매매가 공정거래질서를 저해하 거나 KRX의 시장감시규정을 위배하지 않는 방향으로 알고리즘 시스템을 설계하도록 공지하 였다. 또한 알고리즘 시스템을 이용한 위탁자의 불건전주문을 수탁 받아서는 안 된다고 못 박는 등 알고리즘 시스템의 잦은 매매에 따른 시장 운영부담이 어느 수준이었는지 짐작하게 한다.

재미난 사실 하나. 글을 보면 다음과 같은 문장이 등장합니다. 굵은 글자로 표시한 부분입니다. @dolppi님은 알고 있으려나?(^^)

알고리즘 트레이딩과 관련한 국내 최고의 Blog인 dolppi’s algorithmic Trading에서는 알고리즘 트레이딩을 주문실행전략과 수익추구전략, 그리고 Smart Order Routing으로 정리하고 있다.

1.

알고리즘트레이딩.고빈도트레이딩(High Frequency Trading). 인구에 회자하고 있습니다. 금융투자회사도 같은 듯 다른 이유로 관심을 가지고 있습니다. 몇 일전 어떤 분과 HFT에 대핸 트위터로 이야기할 기회가 있었습니다. 요지는 이렇습니다.

"한국과 아시아에서 HFT는 유의미한 전략이 아니다. 한국에 의미없는 HFT를 소개하고 도입하자고 하는 취지가 이해하기 어렵다"

같은 날 얼굴을 보고 제가 생각하는 바를 설명했죠. 또한 상대방이 말하고자 하는 바를 이해했습니다.그러면서 들었던 생각입니다.

"분명 HFT나 알고리즘트레이딩이라는 단어를 같이 사용하고 있는데 서로 의미하는 바나 사용하는 맥락이 다르구나!!"

그래서 최소한 서로가 대화를 할 때 같은 의미로 사용하자는 취지에서 정리해보았습니다.

2.

우선 증권사에서 펴낸 자료를 따라가면서 알아보도록 하겠습니다. 좀 멀리서 시작해보도록 하죠. Algo Trading이든 HFT이든 기계가 의사결정을 한다는 면에선 시스템트레이딩입니다.시스템트레이딩을 2007년쯤 대신증권에서 정리하였습니다.

위 글에서는 알고리즘 트레이딩을 아래와 같이 정의하고 있습니다.

최근에는 알고리즘 트레이딩(Algorithm Trading)이란 용어의 시스템 트레이딩 방법이 많이 사용되고 있다. 알고리즘 트레이딩이란 자동 주문 시스템이란 의미와 알파(alpha) 수익률 창출을 위한 차익거래 매매의 의미를 내포한 매매형태로서, 대량 주문을 자동으로, 동시 주 문을 자동으로, 분할 주문을 자동으로 설정하는 형태가 많이 사용된다. 주로 기관 투자가가 많이 사용하고 있으며 시스템 매매의 한 분류로 볼 수 있다.

이제 본격적으로 알고리즘트레이딩과 HFT를 어떻게 정의하는지 알아보도록 하겠습니다. 구글링을 해보니까 우리투자증권외 자료를 구하지 못했습니다.

위 글에서는 알고리즘 트레이딩을 다음과 같이 정의합니다.사실 이 정의는 정의로써 문제가 있습니다. 알고리즘트레이딩을 정의하면서 '알고리즘에 의거한"이라는 동어반복을 했기때문입니다.(^^)

알고리즘에 의거한 자동화된 매매를 의미함. 자동화 매매를 이용하는 이유는 거래대상의 가격과 시장 상황 등을 유기 적으로 분석해 해당 알고리즘에 의거한 매매를 최소의 거래비용을 통해 구현하기 위함임. 기본 개념만 놓고 보면 프로그램매매와 매우 유사하며 High Frequency Trading도 알고리즘 트레이딩의 일종으로 볼 수 있음

다음으로 HFT에 대한 정의입니다. 아래글을 유심히 읽어보았지만 HFT에 대한 정의가 매우 막연합니다. 아주 단순화하면 단위시간당 주문건수가 무지무지하게 많다는 정도로 정의하고 있습니다.

High Frequency Trading(이하 HFT)이란 상당히 빈번하게 발생하는 형태의 매매를 의미한다. 컴퓨터 프로그램을 이용한 트레이딩 기법의 일종으로 컴퓨터 성능의 향상과 자동화 기술 의 발달로 가능하게 된 새로운 트레이딩의 형태로 정의 내릴 수 있다.

마지막으로 한국거래소는 어떻게 정의하는지 알아보도록 하겠습니다. 시장감시위원회에서 펴낸 알고리즘트레이딩관련 가이드라인입니다.

위의 가이드라인에서는 다음과 같은 의미로 알고리즘트레이딩을 사용합니다.

알고리즘 트레이딩은 사전에 설정된 매개변수 및 제약조건에 기초해 주문시간과 수량을 자동으로 생성하는 알고리즘을 통해 실행되는 주문 및 거래체계

마찬가지로 시장감시위원회는 HFT를 다음과 같이 정의합니다.

HFT는 IT기술 발달을 기반으로 고도의 프로그램을 통해 수만건의 거래를 일순간에 처리하는 방법으로 초단기간에 호가 상황을 파악하여 주문을 제출하거나 취소하여 초단기이익을 얻는 알고리즘거래의 일환으로 슈퍼컴퓨터를 이용한 알고리즘 트레이딩 기반의 초단기 매매기법

이상이 한국에서 알고리즘트레이딩이나 HFT를 다룬 글의 전부는 아니지만 거래소, 증권회사등의 정의를 살펴보았습니다.

3.

이제 알고리즘트레이딩과 HFT를 어떤 의미로 정의하여야 할까요? 우선 알고리즘트레이딩은 비슷한 내용으로 정리될 듯 합니다.제가 지금까지 본 정의중 2005년에 한 글에서 정리한 아래 문장이 가장 마음에 듭니다.

Algorithmic trading is defined as “placing a buy or sell order of a defined quantity into a quantitative model that automatically generates the timing of orders and the size of orders based on goals specified by the parameters and constraints of the algorithm.

이 말을 우리말로 번역하면 거래소에서 내린 정의와 별반 다르지 않습니다.

알고리즘 트레이딩이란 사전에 설정된 매개변수 및 제약조건에 기초해 주문시간과 수량을 자동으로 생성하는 정략적인 모델(수학적 모델)을 통해 실행되는 주문 및 거래체계

문제는 HFT(High Frequency Trading)입니다. 어떤 분은 '거래횟수'를 강조하는 분도 있고 어떤 분은 '전략 혹은 알고리즘'을 강조하는 분도 계십니다.미국도 명확히 HFT가 무엇인지에 대해 의견이 통일되어 있지 않습니다.

HFT를 140자 이내로 정의하면 - Flash Crash 보고서이후

그렇지만 High Frequency Trading은 1)알고리즘트레이딩이라는 매매기법의 발전 2)HPC(Low Latency등 포함)와 같은 기술적인 진보를 배경으로 하고 있다는 점을 명확히 하여야 합니다.

이를 전제로 HFT를 정의하면

HPC와 Low Latency기술을 기반으로 시장내 유동성의 불균형과 가격의 비효율성으로부터 이익을 얻기 위하여 실시간 호가상황을 판단하여 아주 짧은 시간동안 다량의 주문을 내고 아주 작은 이익을 내는 자동화된 매매전략들

이 아닐까 합니다.

High-frequency trading involves the large-scale turnover of numerous positions, making a small return on each turnover 와

Define high frequency as fully automated trading strategies that seek to benefit from market liquidity imbalances or other short-term pricing inefficiencies. And that goes across asset classes, extending from equities and derivatives into currencies and a little into fixed income을 덧붙인 정의

Breaking it Down: An Overview of High-Frequency Trading중에서

4.

그러면 한국에서 HFT의 가능성을? 먼저 High Frequency라는 말에 연연하지 않았으면 합니다. 무엇이 많다는 기준은 나라마다 시장구조가 다르기때문에 다르다고 생각합니다. KRX관계자가 이런 말을 했습니다.

국내의 경우 단일거래소 체제 및 회원사 시스템을 통한 호가입력방식의 제한으로 알고리즘 트레이딩 등 신매매기법이 활성화되기는 어려울 것이지만 앞으로 이와 관련한 불공정거래 발생 가능성에 대비하겠다

알고리즘 트레이딩등 新매매기법 해외서 활성화중에서

만약 미국처럼 시장이 여러개의 거래소로 나눠졌고 각 거래소간의 가격차이로 부터 기회를 발견하고 코로케이션서비스등으로 Low Latency를 구현하고 막대한 돈을 IT에 투자하는 상황과 비교하면, 한국은 무엇이든 불가능합니다. 그렇지만 Low든 High든 상대적인 개념입니다. KRX의 시장 참여자들을 놓고 비교함이 타당합니다. 하루에 100번 거래를 하고 주문속도가 10ms이하인 상황에서 ELW를 매매하는 슈퍼메뚜기들이 초당 몇 천번, 주문속도가 100마이크로초를 다투는 미국 HFT와 비교하면 HFT가 아니지만 한국내 다른 참여자와 비교하면 HFT라고 할 수 있습니다.

흔히들 HFT를 말할 때 전략이라고 말하는 것들이 있습니다.앞서 우리투자증권의 자료는 다음을 HFT전략이라고 합니다.

1.Flash Orders

2.Liquidity Rebate Trading

3.Market Making

4.Dark Pool Trading

위에서 자료를 소개한 Overview Of HFT를 보면 다음과 같은 전략을 HFT전략이라고 합니다.

1.Market Making

2.Statistical Arbitrage

3.Low Latency Trading

4.Liquidity Detection

5.Flash Orders

Breaking it Down: An Overview of High-Frequency Trading에서는 다음과 같은 전략이라고 합니다.

With arbitrage strategies, Iati explains, traders look to correlate prices between securities in some way and trade off of the imbalances in those correlations. "Those imbalances can and do occur in microsecond time frames," he comments. "The more time that elapses, the more time for those imbalances to be corrected. A trader who can achieve [just] a millisecond of latency can capture some of that opportunity."

Pairs trading, and more specifically cross-asset pairs trading, also is a popular high-frequency trading strategy, according to Iati. "For example, if I am looking at a correlation between Coke and Pepsi -- if one moves up one would expect the other to move up," explains Iati. "Or, in the case of cross-asset pairs, the correlation between the derivative and an underlying asset. So the price of each is tied together. High-frequency traders continuously calculate the value of both, looking for an imbalance."

Another high-frequency strategy is volatility trading or trading on relative price movement rather than absolute price movement. In this case, Iati says, "Traders make money on volatility, not necessarily on movement."

A fourth high-frequency strategy is short-term statistical arbitrage, or a complex form of pairs trading that involves trading a broad range of securities that are correlated, Iati explains. "Stat arb has traditionally been long term, but over the last couple of years that has evolved and it has moved into shorter time frames," says Iati. "Those strategies have been adjusted to take advantage of shorter time horizons, minimizing capital at risk."

The last -- and most controversial -- type of high-frequency trading, according to Iati, is "liquidity detection." "This is when firms are looking to decipher whether there are large orders existing in a matching engine by sending out small orders, or pinging to look for where large orders might be resting," he relates. "When a small order is filled quickly, there is likely to be" a large order behind it.

위의 전략중 Flash Order와 같이 미국 시장구조에 특화된 전략도 있습니다. 반면 Latency Arbitrage와 같이 어느 나라 시장에서도 적용할 수 있는 전략도 있습니다. 슈퍼메뚜기든 ITG와 같은 회사든 상대적으로 많은 거래횟수와 상대적으로 낮은 지연시간(Low Latency)를 이용하여 매매를 한다고 하면 그게 바로 HFT전략이라는 생각입니다.

橘化爲枳(귤화위지).귤이 회수를 건너면 탱자가 된다는 말처럼 미국이나 유럽의 HFT가 물 건너 한국에 와서 한국형 HFT가 되는 것과 같습니다. 이를 테면 Orange(오륀지)가 한국에서 Orange(오렌지)로 된 것처럼(^^)

5.

이제 HFT든 알고리즘 트레이딩이든 확대된다고 예상을 하면 어디에서 출발하여야 할까요? 저는 우선 두가지가 필요하다고 생각합니다.

첫째는 알고리즘개발이나 전략 수립에 필수적인 백테스팅환경을 구축하는 일입니다. 많은 프랍데스크나 부티크는 종가기준으로 모델링하는 듯 합니다. 그렇지만 HFT와 같은 트레이딩은 틱데이타(Tick Based Data)를 기준으로 모델링하여야 합니다.미국 NYSE같은 경우 테라단위 데이타입니다. 몇 년단위의 데이타인지에 따라 다르지만 한국시장은 몇백기가정도가 되지 않을까 합니다. 이런 데이타를 관리하고 분석할 수 있는 데이타관리방안 및 시스템이 구축되어야 합니다.

둘째는 Low Latency환경 구축입니다. Low Latency 혹은 Speed가 트레이딩에 어떤 의미가 있을까요? 차익트레이딩과 펀더멘탈트레이딩은 Low Latency에 대해 다른 의미가 있다고 합니다. 차익트레이딩은 가격정보에 촛점을 두고 순간적으로 발생하는 기회를 포착하는데 목표를 두고 있습니다. 시장에 발 빠르게 대응할 수 있는 환경이 중요합니다. 반면 펀터멘탈트레이딩은 시장에 미치는 영향과 비용을 줄이면서 기회를 포착하는 방식입니다.

Arbitrage driven trading is focused on market data and information. Complex quantitative models are designed to capture temporary opportunities in the marketplace. This trading technique is specifically designed to capture alpha, which can erode within milliseconds. In many cases these models have optimised everything in terms of throughput capacity and the ability to react to changes in information and trading opportunities. At this point of parity, the trader will be left with basic physics – he will have to turn to faster response times rather than changes in information for alpha capture. As latency increases with distance, locating trading technology close to the market centre is the obvious next step in minimising alpha erosion. And at what point does distance make a significant impact in terms of latency? An additional source of arbitrage may be targeting the trading venue itself – by trading the faster venue in order to optimise the relative differences in speeds.

Fundamental trading is opportunistic – unlike the arbitrage-driven trader, the fundamental trader’s main concern is about participating in a fragmented market while minimising impact and delay cost. Most orders are duration orders which may potentially be on the order books right the way through to market close. Alpha erosion over the course of the day is of more importance than split second speed. While latency is not of primary concern, speed is still a key component of best execution and ensuring the capture of liquidity at the best available prices. Venues that enable anonymous trading are becoming more of a feature in this environment, and can be seen in the recent proliferation and popularity of dark liquidity pools. In order to meet their trading objectives, fundamental traders require a solid understanding of order placement methodologies and their broker’s infrastructure and technology.

Check your speed중에서

그런데 미국의 경우 HFT와 펀터멘탈트레이딩의 융합하는 방향으로 나아가야 한다는 의견도 있습니다.

But he argues that to reignite interest in fundamentally driven trading, money managers will have to significantly change the ways they operate – and one way could be to merge HFT and fundamental strategies.

“The current US market structure basically features three types of players. First, the indexers, who allocate capital to passive indices such as the S&P 500. Second, active managers, who employ fundamental analysis. Then HFT, which dominates volumes but acts more like a marketmaker than investor.

“There is nothing, apart from pre-existing policies, to stop fundamental managers incorporating HFT techniques into their own approaches to investment.

“Better returns through creativity are a hallmark of capital markets. Traditional managers will have to adapt, as it is hard to see how the economic backdrop will change any time soon.”

Money managers have to change strategies중에서

어찌되었든 트레이딩에서 Low Latency가 점점더 중요해진다고 사실은 변함이 없습니다. 이미 국내에서도 Latency를 둘러싼 경쟁이 시작되었습니다. KRX가 어떤 정책을 정하든 Low Latency가 증권사의 핵심경쟁력중 하나가 될 것입니다.

6.

마지막으로 KRX의 정책을 보도록 하겠습니다. 금융당국과 KRX는 서로 다른 목표를 지향합니다.금융당국은 투명성,공정성을 지향합니다. KRX는 시장의 성장을 목표로 합니다. 물론 겹치는 부분이 있습니다.

알고리즘트레이딩이나 HFT에 대한 KRX는 규제와 도입사이에서 갈팡질팡 하는 듯 합니다. 우선 KRX 시장감시위원회에서는 체결단위가 아니라 호가단위로 수수료를 부과하는 방안을 도입하겠다고 합니다. 규제책입니다.

투자자들을 현혹하고 전산장애 등을 일으키는 허수성 호가 매매를 막기 위해 ‘체결’에 따라 수수료를 물게 하는 현재의 방식을 ‘호가’에 따라 수수료를 부과하는 미국 방식으로 바꾸는 방안도 함께 검토할 계획이다.

이 철환(55) 한국거래소 시장감시위원장은 지난 5일 서울신문과 가진 인터뷰에서 이렇게 밝히고 “미국, 유럽에서 널리 이뤄지고 있는 컴퓨터 알고리즘 거래가 합리적으로 발전하기 위해서는 호가에 수수료를 붙이는 방식으로 이용자들이 비용을 부담하는 게 맞다고 본다.”고 말했다. 경제관료에서 주식시장의 불공정 거래를 잡아내는 시장감시위원장으로 옮긴 지 3년째를 맞은 그는 요즘 마냥 규제할 수도, 마냥 풀어줄 수도 없는 알고리즘 거래의 균형점을 찾는 데 고심하고 있다고 했다.

“폐단 많은 극초단타 매매 하루 주문수량 제한 검토” 중에서

반대로 시중에 공개하지 않고 언론사 기사들에게 제공한 보고서는 허용이라는 입장을 보여줍니다. 아래 글중에 '해외 신매매기법 현황 및 시사점'라는 자료를 찾으려고 노력했지만 기사도 없다고 하네요.(^^;)

그런데 지난 23일, 거래소는 '해외 신매매기법 현황 및 시사점'이라는 자료를 통해 "해외거래소의 경우 알고리즘 거래, 고주파매매를 규제하기보다 오히려 장려하는 상황"이라고 태도를 바꿨다. "특히 HFT는 현재 불공정 관련 문제점이 없다"고 아예 단정지었다.신종 IT기술을 동원한 거래기법 도입을 주시하고 지속적으로 감시하겠다던 거래소가 '감시'보다는 '장려'쪽으로 돌아선 것이다.

한국거래소의 수익마인드중에서

아래에서도 '알고리즘 매매 수용을 위한 시장관리 방안'이라는 보고서가 나옵니다만 확인이 불가능합니다.

우리나라 거래소는 어떤가. SEC의 규제 논의가 벌써 작년 9월에 시작되었는데도 거래소는 1년이 지난 10월에야 태스크포스를 가동했다. 그 사이 국내 한 증권사는 외국인 기관투자가를 대상으로 극초단타 매매 서비스를 시작했다. 국감장에서 방지 대책을 제대로 수립하지 못하고 있다는 질타를 받기도 했다.

대책을 마련하겠다는 거래소는 기자에게 '알고리즘 매매 수용을 위한 시장관리 방안'이라는 보고서를 보내왔다. 극초단타 매매를 포함하는 알고리즘 매매를 피할 수 없는 세계적인 조류로 판단하고 있었다. 물론 알고리즘 매매와 관련한 규제 강화 내용도 담겨 있다. 그러나 '수용'을 전제로 한 보고서의 진정성에 대해서는 의문이 여전히 남을 수밖에 없다.

극초단타매매와 한국의 현실중에서

KRX가 샌드위치가 된 듯 합니다. 규제를 바라는 감독당국와 허용을 바라는 업계의 요구사이에서 갈팡질팡하는 듯 합니다.

이런 글이 기억납니다. 미국 투자은행은 볼커룰로 돈줄인 프랍트레이딩을 할 수 업게 되었습니다. 또한 여러가지로 규제가 많아서 예전처럼 운용할 수 없다고 합니다. 그래서 지하(Going undergroud)로 숨는다고 합니다. 한국으로 말하자만 사설 헤지펀드나 사모펀드같은 식으로 간다고 합니다.

시장에 이익을 보려는 사람은 무슨 수를 쓰더라도 방법을 찾습니다. 막는다고 막히진 않습니다.

7.

이 글을 보다 몰랐던 사실을 알았습니다. 이전에 KRX 시장감시위원회에서 펴낸 자료에서 짐작은 했지만 공문으로 내려보낸 줄을 몰랐습니다. 그래서 위에 PDF로 변화하여 올려놓았습니다.

지 난 5월 18일 KRX는 공문을 통해 알고리즘 트레이딩과 관련한 가이드라인을 제시했다. 알 고리즘 트레이딩 과정에서 발생하는 허수성 호가 및 가장성 매매가 공정거래질서를 저해하 거나 KRX의 시장감시규정을 위배하지 않는 방향으로 알고리즘 시스템을 설계하도록 공지하 였다. 또한 알고리즘 시스템을 이용한 위탁자의 불건전주문을 수탁 받아서는 안 된다고 못 박는 등 알고리즘 시스템의 잦은 매매에 따른 시장 운영부담이 어느 수준이었는지 짐작하게 한다.

재미난 사실 하나. 글을 보면 다음과 같은 문장이 등장합니다. 굵은 글자로 표시한 부분입니다. @dolppi님은 알고 있으려나?(^^)

알고리즘 트레이딩과 관련한 국내 최고의 Blog인 dolppi’s algorithmic Trading에서는 알고리즘 트레이딩을 주문실행전략과 수익추구전략, 그리고 Smart Order Routing으로 정리하고 있다.

2010년 11월 7일 일요일

Latency measurement takes a step forward

Fri, 2010-11-05 14:32 - The Trade News

The Chicago Board Options Exchange (CBOE) and Interactive Data have both invested in new latency management tools, aimed at increasing trading performance and transparency for trading firms.

US derivatives venue CBOE has opted for the RaceTeam service offered by latency measurement firm Correlix. RaceTeam enables trading firms to manage and receive real-time latency intelligence information from various trading venues. The offering will enable the CBOE to provide latency insight data in real time to its customers on both its existing exchange as well as its all-new C2 Options exchange.

“This service will help our customers better understand how their orders are being processed and, ultimately, we feel that this added degree of transparency will help them trade on CBOE even more effectively than they do currently,” said Gerald O’Connell, CIO and executive vice president of systems at CBOE.

RaceTeam is expected to begin processing the CBOE latency data later this year.

Meanwhile, US-based data provider Interactive Data has launched its 7ticks latency portal, which is designed to serve as a one-stop centralised resource for electronic traders to measure latency, monitor network performance and determine the overall health of their trading infrastructure.

Through the latency portal, clients can access services available from a variety of technology providers to obtain data related to multi-tier infrastructure performance, latency analysis and metrics, as well as multi-tier order analysis. With the launch of the latency portal, Interactive Data also offers business intelligence and a variety of customer service options.

Business intelligence functions range from analysis tools and a customisable dashboard, as well as cross-tool data correlation and proactive analytics. The customer service capabilities include product update and enhancement notification, trouble ticket visibility, market and financial news and inventory management.

Interactive Data 7ticks provides managed ultra-low latency services to facilitate electronic trading. These services include co-location, proximity hosting, direct market access, monitoring, ultra-low latency infrastructure, connectivity and support.

The Chicago Board Options Exchange (CBOE) and Interactive Data have both invested in new latency management tools, aimed at increasing trading performance and transparency for trading firms.

US derivatives venue CBOE has opted for the RaceTeam service offered by latency measurement firm Correlix. RaceTeam enables trading firms to manage and receive real-time latency intelligence information from various trading venues. The offering will enable the CBOE to provide latency insight data in real time to its customers on both its existing exchange as well as its all-new C2 Options exchange.

“This service will help our customers better understand how their orders are being processed and, ultimately, we feel that this added degree of transparency will help them trade on CBOE even more effectively than they do currently,” said Gerald O’Connell, CIO and executive vice president of systems at CBOE.

RaceTeam is expected to begin processing the CBOE latency data later this year.

Meanwhile, US-based data provider Interactive Data has launched its 7ticks latency portal, which is designed to serve as a one-stop centralised resource for electronic traders to measure latency, monitor network performance and determine the overall health of their trading infrastructure.

Through the latency portal, clients can access services available from a variety of technology providers to obtain data related to multi-tier infrastructure performance, latency analysis and metrics, as well as multi-tier order analysis. With the launch of the latency portal, Interactive Data also offers business intelligence and a variety of customer service options.

Business intelligence functions range from analysis tools and a customisable dashboard, as well as cross-tool data correlation and proactive analytics. The customer service capabilities include product update and enhancement notification, trouble ticket visibility, market and financial news and inventory management.

Interactive Data 7ticks provides managed ultra-low latency services to facilitate electronic trading. These services include co-location, proximity hosting, direct market access, monitoring, ultra-low latency infrastructure, connectivity and support.

HFT와 관련한 두가지 뉴스

2010/03/28 15:36 - 그대안의 작은 호수

1.

Traders Piqued By the Picosecond, But Physics Intervenes

Wall Street’s fastest traders have their eyes set on the newest speed–the picosecond, or one trillionth of a second. But even as trading reaches its fastest levels yet, companies with the need for speed are running into a pesky problem: the speed of light.

“When you look at what you need to do to get a trade from a firm to the exchange and back, there are other things involved–like physics–that make it difficult,” said Mark Palmer, president of StreamBase Systems, which develops trading tools and platforms. “When you get to that level, you are starting to approach speed-of-light problems.”

While no one is actually executing trades in the span of one picosecond yet, the race is on to start clocking parts of a trade in this smallest of measurements. Engineers are now working on getting a single chip inside a computer’s central processing unit, for instance, to run at their fastest speeds yet.

Adam Sussman, director of research at TABB Group, said people aren’t measuring the trading process in picoseconds. But “if you begin to slice your process into ever-more granular steps, you start to see things in picoseconds,” he said.

In order to stay competitive, many are paying to rent space within or near the exchanges, a practice called co-location.

StreamBase, founded by MIT engineers, follows a similar approach. “We hired 40 engineers and have them think really hard,” Palmer said. “Five years ago, five milliseconds was actually fast. Now, five milliseconds is really slow. It means there’s a bug in your system.

No we are hiring engineers to figure out how to trade in picoseconds. Why is this speed necessary? Why is our industry spending billions of dollars on technology to achieve this speed? Will this spending result in picking stocks to buy at $10 that will appreciate to $50? Will this result in new public small-cap capital formation? No

This will result in larger brokerage firms and hedge funds getting even larger by beating long term investors to a quote. Legalized stealing. Having fun?

If you ask an exchange developer, they’ll likely tell you that the physics (speed of light, materials of components, etc.) make 100 microsecond speeds a theoretical limit. To be talking picoseconds — a millionth of a micro — you either can’t do math (ok, ok; I know we’re talking TABB here), or you’re assuming that HFT strategies will be driven by microchips that will sit INSIDE of exchange matching engines.

On the math: the speed of light travels .3 millimeters in a picosecond. So that pretty much takes networks out of the picture.

On intra-matching engine co-lo: Today, most exchanges split matching engines across symbols to enhance performance — in other words, they throw more servers at the problem to gain speed. (Nasdaq is the lone exception that I’m aware of; there’s an ongoing debate as to whether they’ll have to change this architecture in the future.) Can exchanges “beef up” matching engines to accomodate co-lo’ed chips from users — maybe by further splitting symbols (and thereby increasing operating costs)? Maybe. Would the SEC allow it? Maybe. Does the entire notion scream “decreasing marginal benefits?” Absolutely. (Unless you’re a technology vendor or a consulting firm trying to sell people stuff.)

2. High Frequency Equities Trading: From the U.S. to Asia?

However, lacking precise data, our proxy for strategy is strong sensitivity to latency in the trading process. Today, our research suggests that latency-sensitive trading is highly pervasive and as a result we estimate that 42% of U.S. equities volume (measured in shares) is the result of HFT and will grow to 54% of volume by 2010.

A higher penetration of HFT will be multi-faceted and driven by an increase in the number of proprietary trading firms, an expansion of quantitative hedge fund strategies, and increasingly technology-driven automated market making. In addition, the convergence of fundamental and quantitative strategies by investment firms will mean the coupling of execution and investment strategies, leading to greater HFT adoption among even more traditionally conservative organizations. In other words, a rising HFT tide will lift all boats.

Back to the rest of the world. The adoption of HFT in Europe is less as a percentage of order flow than the U.S., but is growing. At the same time, HFT will most certainly expand in Asia over the next several years, with selected Asian marketplaces like Tokyo, Singapore, Hong Kong and Australia with the most potential for evolutionary changes at present. With the major upgrade of the Tokyo Stock Exchange's new Arrowhead system, the number of HFT firms trading Japanese equities will grow significantly. We also expect that Arrowhead will spur other innovations and compel more U.S. and European firms to locate trading applications closer to the exchange matching engines in Tokyo.

Similarly, these firms may also move to be physically closer to other Asian exchange matching engines. However, as a result of more heavy-handed regulation, culture and vested interests, the equities market structure in Asian markets should be slower to evolve than Europe post-MiFID introduction. Hence, we expect the HFT growth trajectory will not accelerate to the levels seen in U.S. and Western Europe anytime soon.

3.

HFT는 지역적으로, 기술적으로 한계에 도전하고 있습니다. 지역적으로 금융중심에서 부심으로 영역을 넓혀가고 있습니다. Latency에서도 불가능하고 의미가 없을런지 몰라고 피코초(秒)에 도전하고 있습니다. 이런 상황에서 KRX는 고객의 무관심으로 HFT가 한국에 도입되지 못하고 있다는 뉘앙스로 이야기하고 있습니다.

국내 알고리즘 트레이딩 성공 가능성

물론 알고리즘 트레이딩과 HFT를 같은 범주로 생각할 수 없지만 어느 정도 동전의 양면이라고 생각합니다. 어떤 알고리즘보다 가장 확실한 알고리즘은 Latency Arbitrage라고 생각하기 때문입니다. 이 점을 이용한 매매가 고빈도 매매 즉, HFT입니다.

1.

Traders Piqued By the Picosecond, But Physics Intervenes

Wall Street’s fastest traders have their eyes set on the newest speed–the picosecond, or one trillionth of a second. But even as trading reaches its fastest levels yet, companies with the need for speed are running into a pesky problem: the speed of light.

“When you look at what you need to do to get a trade from a firm to the exchange and back, there are other things involved–like physics–that make it difficult,” said Mark Palmer, president of StreamBase Systems, which develops trading tools and platforms. “When you get to that level, you are starting to approach speed-of-light problems.”

While no one is actually executing trades in the span of one picosecond yet, the race is on to start clocking parts of a trade in this smallest of measurements. Engineers are now working on getting a single chip inside a computer’s central processing unit, for instance, to run at their fastest speeds yet.

Adam Sussman, director of research at TABB Group, said people aren’t measuring the trading process in picoseconds. But “if you begin to slice your process into ever-more granular steps, you start to see things in picoseconds,” he said.

In order to stay competitive, many are paying to rent space within or near the exchanges, a practice called co-location.

StreamBase, founded by MIT engineers, follows a similar approach. “We hired 40 engineers and have them think really hard,” Palmer said. “Five years ago, five milliseconds was actually fast. Now, five milliseconds is really slow. It means there’s a bug in your system.

No we are hiring engineers to figure out how to trade in picoseconds. Why is this speed necessary? Why is our industry spending billions of dollars on technology to achieve this speed? Will this spending result in picking stocks to buy at $10 that will appreciate to $50? Will this result in new public small-cap capital formation? No

This will result in larger brokerage firms and hedge funds getting even larger by beating long term investors to a quote. Legalized stealing. Having fun?

If you ask an exchange developer, they’ll likely tell you that the physics (speed of light, materials of components, etc.) make 100 microsecond speeds a theoretical limit. To be talking picoseconds — a millionth of a micro — you either can’t do math (ok, ok; I know we’re talking TABB here), or you’re assuming that HFT strategies will be driven by microchips that will sit INSIDE of exchange matching engines.

On the math: the speed of light travels .3 millimeters in a picosecond. So that pretty much takes networks out of the picture.

On intra-matching engine co-lo: Today, most exchanges split matching engines across symbols to enhance performance — in other words, they throw more servers at the problem to gain speed. (Nasdaq is the lone exception that I’m aware of; there’s an ongoing debate as to whether they’ll have to change this architecture in the future.) Can exchanges “beef up” matching engines to accomodate co-lo’ed chips from users — maybe by further splitting symbols (and thereby increasing operating costs)? Maybe. Would the SEC allow it? Maybe. Does the entire notion scream “decreasing marginal benefits?” Absolutely. (Unless you’re a technology vendor or a consulting firm trying to sell people stuff.)

2. High Frequency Equities Trading: From the U.S. to Asia?

However, lacking precise data, our proxy for strategy is strong sensitivity to latency in the trading process. Today, our research suggests that latency-sensitive trading is highly pervasive and as a result we estimate that 42% of U.S. equities volume (measured in shares) is the result of HFT and will grow to 54% of volume by 2010.

A higher penetration of HFT will be multi-faceted and driven by an increase in the number of proprietary trading firms, an expansion of quantitative hedge fund strategies, and increasingly technology-driven automated market making. In addition, the convergence of fundamental and quantitative strategies by investment firms will mean the coupling of execution and investment strategies, leading to greater HFT adoption among even more traditionally conservative organizations. In other words, a rising HFT tide will lift all boats.

Back to the rest of the world. The adoption of HFT in Europe is less as a percentage of order flow than the U.S., but is growing. At the same time, HFT will most certainly expand in Asia over the next several years, with selected Asian marketplaces like Tokyo, Singapore, Hong Kong and Australia with the most potential for evolutionary changes at present. With the major upgrade of the Tokyo Stock Exchange's new Arrowhead system, the number of HFT firms trading Japanese equities will grow significantly. We also expect that Arrowhead will spur other innovations and compel more U.S. and European firms to locate trading applications closer to the exchange matching engines in Tokyo.